Every building begins somewhere else. The sand in its concrete, the stone on its façade, the lithium that may one day power its systems. It arrives, already stripped from a mountain, a riverbed, or a salt flat thousands of kilometers away, having passed through a chain of trucks, ships, and customs declarations that erase almost everything about where it came from. Architecture tends to treat material as a starting condition, something simply available, but extraction is where construction actually begins.

The global trade in construction sand alone now moves on a scale that rivals the illegal markets in timber, gold, and fish combined, run through networks violent enough to have cost reporters and activists their lives. A single mountain in Tuscany has yielded more marble in the past few decades than in the two thousand years before them, hollowed out by a workforce whose own history of revolt has been almost entirely forgotten. Beneath the salt flats of three South American countries and the copper belt of Central Africa, the minerals that will supposedly power a cleaner future are pulled from ground that Indigenous communities have inhabited for generations and that children, in some cases, mine by hand. Each of these is sold as ordinary commerce; each is also a territorial transaction whose terms were set somewhere far from where the material was taken.

What connects sand, stone, and critical minerals is not only the distance they travel, but who was already living where they were removed from, and how little say that population had in the transaction. A riverbank community in Cambodia, a quarry town in the Apuan Alps, an Indigenous family watching a valley dry up in Argentina. None of them signed the contract that determined what would happen to their ground. To understand a marble façade, a poured concrete slab, or a battery pack only in terms of its finish is to accept the most depoliticized version of a story that is, at every stage, about who controls ground and who is forced to leave it.

Related Article

Unearthing the Ground: Architecture and the Politics of Oil

The Sand Trade

The world consumes up to fifty billion metric tons of sand every year, making it the largest extraction industry on the planet (projected to rise by up to 45% by 2060). Desert sand, eroded by wind into smooth, rounded grains, cannot bind concrete; construction depends on the sharp, angular sand carried by rivers and coastlines, which means an entire industry sits beside a resource it cannot use and must instead extract from somewhere. That contradiction, abundance next to scarcity, has turned an unglamorous building material into a commodity worth fighting, bribing, and occasionally killing for.

A federal police specialist in Brazil who studies extractive industries estimates the global illegal sand trade at between two hundred and three hundred and fifty billion dollars a year (more than illegal logging, gold mining, and fishing combined), yet sand draws almost no scrutiny because it looks like an ordinary, unglamorous resource, and because legal and black-market are visually indistinguishable once they reach a construction site. In India alone, illegal sand mining has become the country’s largest organized criminal activity, with hundreds of people killed in recent years in conflicts connected to it. Among them, in 2019, a journalist was murdered for reporting on the corruption behind it. India’s demand for sand tripled between 2000 and 2017, and the country now needs to add eight hundred million square meters of urban space every year just to keep pace with housing demand. A treadmill that keeps the trade lucrative regardless of how many regulations are introduced to slow it.

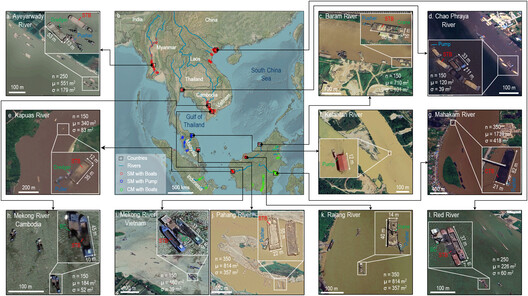

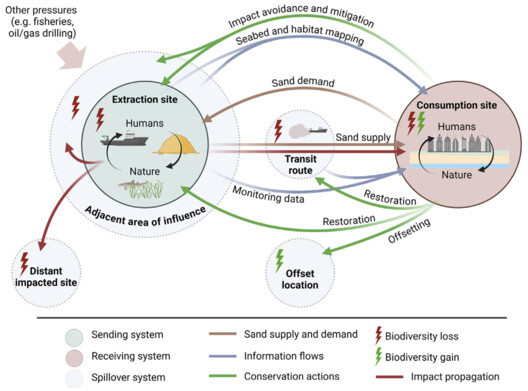

The geography of who supplies and who consumes is just as politically charged as the violence surrounding it. In Southeast Asia, the sand trade has produced a state-level dispute between Singapore, which imports the material, and Malaysia, which has restricted its export. Singapore’s land reclamation needs have led to sand being dredged illegally from Cambodia and Indonesia on an industrial scale, turning one country’s territorial expansion into another’s slow disappearance. The lower Mekong basin shows that exchange, where sand mining is most intensive in Cambodia and Vietnam, driven by the construction boom of a rapidly urbanizing Southeast Asia, and where the river’s six riparian nations have little say over a trade shaped as much by geopolitical rivalry as by domestic demand. Singapore’s reclaimed shoreline is, in this sense, a transferred geology, a new land built from someone else’s riverbank, legally purchased but politically extracted.

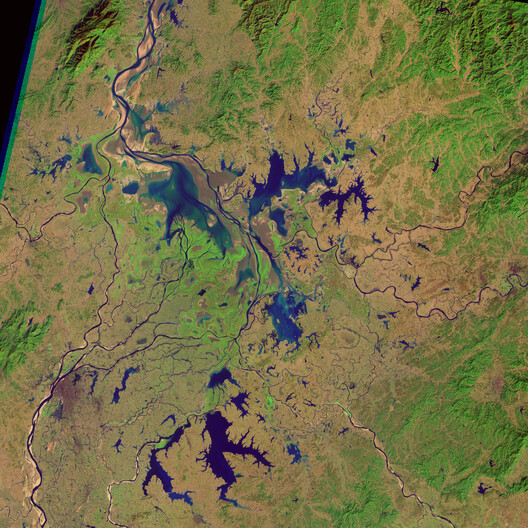

An independent ecologist studying the Mekong Delta has argued that sand is classified merely as an ordinary construction material under mining law, even though it plays a structural role in maintaining the territory itself. Meaning that continued extraction at current rates could force the map of the delta to be redrawn as its coastline erodes and its riverbanks deform.

In sand-rich extraction zones, people face displacement as riverbanks erode and homes collapse into the water, while the economic gains concentrate in distant, wealthier cities far from the site of extraction. The depletion reaches further than the riverbank, sand mining also draws down the water table, pushing distressed farming communities into the cities whose construction depends on the very extraction that displaced them, a cycle that feeds rising urbanization with the casualties of its own supply chain.

What makes sand different from oil is precisely its appearance of innocence. Buyers rarely check where their sand came from, because there is no property owner to lodge a complaint and no visible difference between a legal truckload and a stolen one. A building’s foundation, in other words, can be the end point of a trade as violent and as poorly governed as any other extractive industry, it simply arrives looking like nothing more than ground.

Carved and Shipped

More marble has been removed from Carrara in recent decades than in the previous two thousand years combined, with annual extraction now reaching around four million tons, dwarfing the few hundred thousand tons a year typical of the early twentieth century.

The Apuan Alps above the town show evidence of at least 650 separate quarry sites, more than the 276 quarries currently producing any kind of natural stone across the entire United States, a country roughly three hundred times Carrara’s size.

The labor that made that extraction possible has its own political history. By the end of the nineteenth century, Carrara had become a center of anarchism in Italy, particularly among its quarry workers, many of whom were ex-convicts or fugitives, employed because the work was arduous enough that almost no one else would take it. Workers eventually rose up against those conditions, organizing along anarchist lines (the Lunigiana revolt), and the Italian state crushed the uprising so thoroughly that many Carrara quarrymen emigrated to the United States, finding work instead in the marble and granite quarries of Vermont. The connection did not end with that one generation; two companies headquartered in Carrara, R.E.D. Graniti and Mazzucchelli Marmi, now own and operate Vermont’s Danby quarry, the largest underground marble quarry in the world.

The marble does not stay in Carrara, and neither did the men who once worked it never had any lasting claim on what they extracted. Large blocks are shipped abroad, where cheaper labor produces tiles, furniture, and luxury finishes, and the town that was once the beating heart of marble craftsmanship has lost nearly all of its own artisanal industry as a result. China has become one of the largest buyers of raw blocks, taking in more than half of certain export categories, while the United States remains a top market for the finished slabs, tiles, and custom pieces that come back the other way. A material literally formed by the compression of an entire mountain range now travels twice around the planet’s supply chains before it lands in a kitchen. The proof, again, that what is expensive about marble is no longer just the stone, but the geography it is forced to pass through on its way to becoming a surface

Marble dust generated by the extraction process infiltrates the region’s aquifers, rendering water undrinkable, while quarry-eroded slopes become geologically unstable, intensifying the risk of mudslides and floods in the surrounding valleys, hazards that have already caused major displacement, including a 2014 flood that left four hundred people needing rescue. Anna Marson, a former Tuscany regional minister, helped put forward a 2014 plan for stricter environmental regulation of the quarries, only to face what she has described as a sustained campaign by quarry owners, who bought entire newspaper pages to oppose her.

The Salt Flat Beneath the Battery

If sand and stone represent the oldest forms of extraction, the minerals driving the energy transition represent its newest and most ideologically complicated chapter. Global lithium production will need to grow more than fivefold by 2030 to meet net-zero targets, requiring well over a hundred billion dollars in new investment. That growth is reshaping landscapes, and wondering what is an acceptable cost for the mineral that promises to lower everyone else’s emissions?

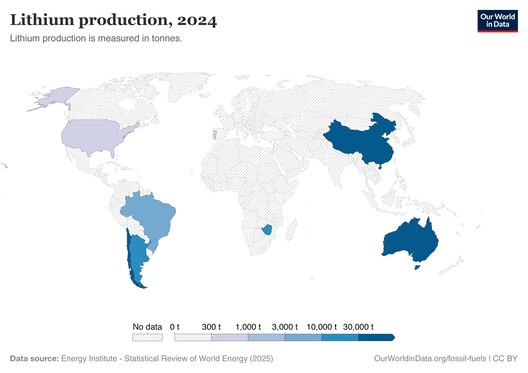

Argentina, Bolivia, and Chile together control more than half of the world’s known lithium resources, concentrated in the brine deposits beneath their shared high-altitude salt flats, with Chile alone holding roughly a quarter of the global reserve base, much of it in the Salar de Atacama, ancestral territory of the Lickanantay people. Extraction, here, means pumping ancient underground brine to the surface and spreading it across evaporation ponds that can stretch for thousands of hectares, where the water disappears into the desert air and leaves the lithium behind. The brine method consumes between roughly four hundred fifty thousand and six hundred fifty thousand liters of water for every ton of lithium carbonate produced, and in the Atacama, mining companies have been accused of depleting up to sixty-five percent of the region’s vital water supplies (water that took thousands of years to accumulate and will not return on any human timescale).

An Indigenous activist who grew up beside Argentina’s oldest lithium mine, at the Salar del Hombre Muerto, has described what that depletion looks like at the scale of a single family. His household once raised llamas, goats, and sheep along a river that lithium production has since diverted and dried, leaving a valley that, in his words, was once beautiful. Today has no animals because it is all dry. Satellite analysis by researchers at the University of Chile has given versions of that damage, identifying ground deformations across the Atacama salt flat that show subsidence concentrated precisely where extraction is heaviest. Sonia Ramos Chocobar has summarized the stakes more starkly: the salt flat, she said, is now on death row.

But not all lithium comes from a desert, and the alternative carries its own ledger of trade-offs. Hard-rock sources, concentrated mainly in Australia, account for around sixty percent of the world’s mined lithium supply, extracted as spodumene ore from open-pit mines rather than pumped as brine. Hard-rock mining requires far less water than brine extraction, an increasingly important advantage as global water scarcity intensifies, but it carries a substantially higher carbon footprint (roughly fifteen to twenty-five kilograms of CO2-equivalent per kilogram of lithium carbonate, compared to five to fifteen for brine, making hard-rock lithium on average three times more carbon-intensive than its desert counterpart).

Mining itself accounts for only around fifteen percent of that footprint; the remaining eighty-five percent comes from downstream processing, much of which, despite originating in Australia, takes place in China, adding a further leg of transcontinental shipping to the mineral’s carbon ledger before it ever reaches a battery factory. The choice between a drained aquifer in the Atacama and a coal-linked processing plant tied to an open-pit mine in Western Australia is not a choice between harm and no harm; it is a choice about which landscape, and which kind of damage, the energy transition is willing to make.

The economics of who controls that ground are shifting as fast as the demand driving it, and not always toward the communities living above it. Chile is moving toward partial state control, with a new partnership between the state mining company Codelco and the private producer SQM giving the government a majority stake, alongside negotiations to include Atacameño communities in industry governance. Bolivia has taken the opposite route, fast-tracking a billion-dollar, state-controlled deal with Chinese investors to build new lithium plants, an agreement so contested domestically that it triggered a chaotic congressional session of shouting and open protest from lawmakers opposed to deals with Chinese and Russian firms. Argentina has chosen a third model, courting private and foreign capital under favorable investment terms, making regional coordination among the three countries unlikely given how differently each has decided to govern the same mineral. The cost differences reinforce these divergent strategies as Australian hard-rock lithium carbonate is projected to cost between roughly $7,800 and $9,200 per metric ton in 2026, compared to $5,800 to $7,000 for Argentina’s brine-based production.

The same battery depends on an entirely different geography for its other critical mineral. The Democratic Republic of the Congo holds an estimated seventy percent of the world’s cobalt reserves, much of it extracted through artisanal and small-scale mining across the country’s mineral-dense Copper Belt (a work that provides essential income for local families but carries severe health, safety, and environmental risks). Roughly eighty percent of the DRC’s cobalt is owned by Chinese companies, refined in China, and sold on to battery makers worldwide, meaning the mineral crosses the planet twice, as raw ore and again as finished cell, before reaching a vehicle showroom.

The U.S. Department of Labor estimates at least twenty-five thousand children work in the country’s cobalt mines, and labor investigations at several industrial sites, including Chinese-owned operations, have documented adult workers laboring in extreme hardship for wages as low as two dollars a day. Aid organizations working in the mining communities describe a harder economic truth, as families depend overwhelmingly on women’s income, and when mothers struggle to provide, children step in. Programs aimed simply at removing children from the mines risk displacing them into even more precarious work if they do not also address the poverty driving the decision in the first place.

What Travels, What Stays

Every material in this article moved twice: once out of the ground, and once again into a story about progress, design, or necessity. A building’s bill of materials is, in this sense, also a map, of quarries, riverbeds, and salt flats most of its occupants will never see, and of the people who were asked, one way or another, to make room for what the rest of the world wanted to build.

Architecture’s growing interest in circularity and material honesty has so far stopped short of the harder question underneath it: not how a material performs once it reaches the site, but what it cost the place it left behind, and who was made to move so that the rest of us could stay still.

This article is part of the ArchDaily Topic: Architectures of Movement: Land, Borders, and the Politics of Belonging. Every month we explore a topic in-depth through articles, interviews, news, and architecture projects. We invite you to learn more about our ArchDaily Topics. And, as always, at ArchDaily we welcome the contributions of our readers; if you want to submit an article or project, contact us.